Monetary Policy

|

|

|

|

|

| Overview | Policy Announcement Tracker | Framework | Decision Making/ Formulation Process | Calendar | Instruments/ Tools | Reports/ Publications | FAQ |

Overview

What is Monetary Policy ?

Monetary policy is the process by which the central bank influences the cost (i.e., interest rate) and availability of money (i.e., money supply/liquidity) with a view to attaining price stability.

Central Bank of Sri Lanka is responsible for conducting monetary policy in Sri Lanka, which mainly involves setting the policy interest rates and managing the liquidity in the economy. The monetary operations of the Central Bank influence interest rate in the economy, affecting the behavior of borrowers and lenders, economic activity and ultimately the rate of inflation. Therefore, the Central Bank uses monetary policy to control inflation and keep it within a desired path.

Price Stability

Price stability is a situation where there are no wide fluctuations in the general price level in the economy, which helps to achieve sustainable economic growth. When the prices fluctuate at a low rate, they would not have any significant influence on the economic decisions of agents of the economy, viz. households and firms. Moreover, price stability helps better anchor inflation expectations among the public, which in turn makes it easier to keep actual inflation at low and stable levels. Therefore, stable prices would not distort the economic decisions regarding what to produce and how to produce, thus enabling efficient allocation of resources in the economy leading to economic stability and sustainable growth in the economy over the longer term. Accordingly, as per the Central Bank of Sri Lanka Act, No.16 of 2023 (CBA), the Central Bank, in pursuing its primary objective of achieving and maintaining domestic price stability, shall also take into account, inter alia, the stabilisation of output towards its potential level.

Policy Announcement Tracker

| Announcement No. | Meeting Date | Announcement Date | Materials | Monetary Policy Report |

| 2025/05 | Tuesday, 23rd September 2025 | Wednesday, 24th September 2025 |

Monetary Policy Report - February 2026

|

|

| 2025/06 | Tuesday, 25th November 2025 | Wednesday, 26th November 2025 | ||

| 2026/01 | Tuesday, 27th January 2026 | Wednesday, 28th January 2026 | ||

| 2026/02 | Tuesday, 24th March 2026 | Wednesday, 25th March 2026 |

|

|

| 2026/03 | Monday, 25th May 2026 | Tuesday, 26th May 2026 | ||

| 2026/04 | Tuesday, 21st July 2026 | Wednesday, 22nd July 2026 |

Presentation Video |

|

| 2026/05 | Tuesday, 29th September 2026 | Wednesday, 30th September 2026 | ||

| 2026/06 | Thursday, 19th November 2026 | Friday, 20th November 2026 | ||

| 2027/01 | To be announced | To be announced |

Policy Announcement Tracker - 2025

Framework

The Central Bank conducts monetary policy to achieve its primary objective of maintaining domestic price stability. According to the CBA, the Monetary Policy Board is responsible for formulating monetary policy and implementing a flexible exchange rate regime in line with the Flexible Inflation Targeting (FIT) framework. The FIT framework aims to maintain inflation at targeted levels as determined by the Monetary Policy Framework Agreement (MPFA) between the Minister of Finance and the Central Bank. The current MPFA, published in the Government Gazette on 5 October 2023, mandates the Central Bank to maintain quarterly headline inflation at 5 per cent.

To achieve the inflation target, the Central Bank uses its policy instruments to guide short term interest rates along the desired path. The Overnight Policy Rate (OPR), which is the primary monetary policy instrument that signals the Central Bank’s monetary policy stance, is periodically reviewed and adjusted appropriately, if necessary, to guide short-term interest rates in the money market. The Average Weighted Call Money Rate (AWCMR), which is a short-term money market interest rate, functions as the operating target under the current monetary policy framework. Further, Open Market Operations (OMOs) are also conducted to manage liquidity conditions in the domestic money market to steer short-term interest rates toward desired levels. Standing Facilities are available for those participating financial institutions that were unable to obtain their liquidity requirements at the daily auction.

Prior to the introduction of OPR, the rates of the Standing Facilities, i.e., the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR), served as policy interest rates of the Central Bank. Previously, the Central Bank conducted monetary policy within an enhanced monetary policy framework with features of both monetary targeting and flexible inflation targeting (FIT). Under this framework, the Central Bank attempted to stabilise inflation at mid single digit levels. Similar to the current practice, AWCMR was used as the operating target. During early 1980s, the Central Bank adopted monetary targeting as its monetary policy framework, and monetary aggregates were the key nominal anchors in the conduct of monetary policy. Under a monetary targeting framework, the changes in money supply are considered the primary causal factors affecting price stability. However, given the rising volatility in the money multiplier and velocity amid a weakening relationship between money supply and inflation, the role of monetary targets as a nominal anchor became uncertain and also complicated the Central Bank’s communication strategy, causing the Central Bank to upgrade its monetary policy framework.

|

|

| Central Bank of Sri Lanka Act (CBA)

|

Monetary Policy Framework |

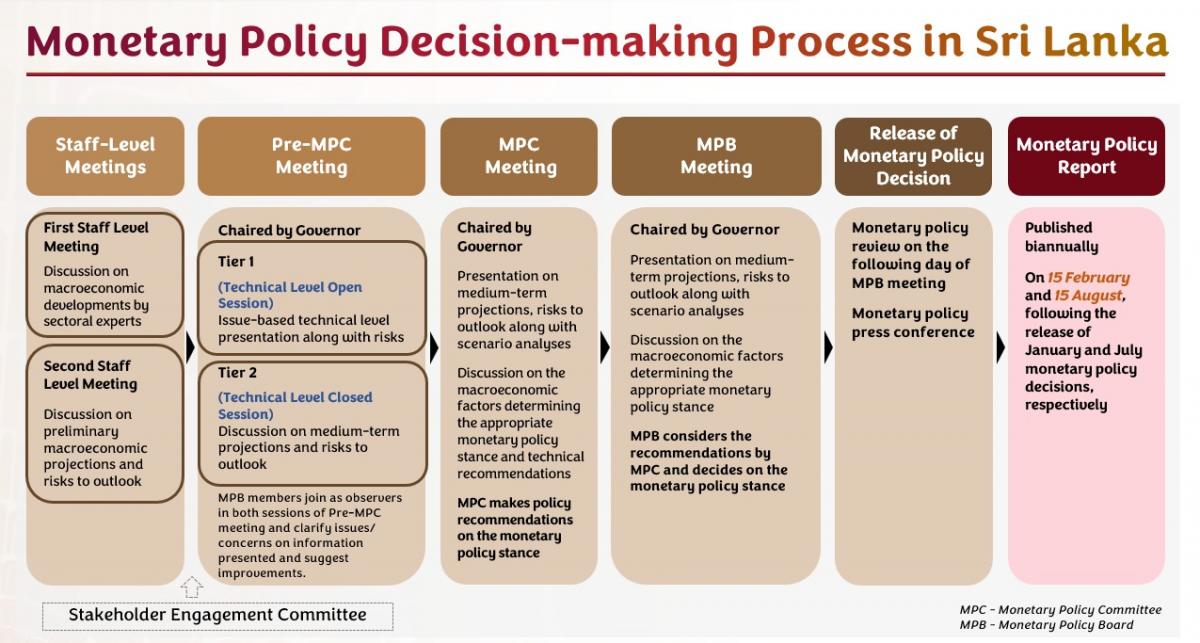

Decision Making/ Formulation Process

Monetary Policy Committee (MPC)

A primary function of the Central Bank, as stated in the CBA, is the determination and implementation of monetary policy for the country. Over the years, the economy, and in particular the financial sector has strengthened and become sophisticated along with the financial sector reforms and structural changes in the economy. Consequently, the Central Bank's tasks in determining and implementing monetary policy have also increased in complexity. Hence, as a part of the Central Bank's efforts to strengthen monetary policy analysis and formulation and as a step towards improving the transparency of the decision-making process, a formal Monetary Policy Committee (MPC) was established in early 2001.

Currently, the Monetary Policy Committee (MPC) is chaired by the Governor and comprises the following members:

Chairperson

- Governor

Members

- All Deputy Governor/s

- Assistant Governor/s in charge of the Departments of Economic Research, Statistics and Market Operations

- Director of Economic Research

- Director, Statistics

- Director, Market Operations

- Additional Director of Economic Research overseeing Money and Banking

- Secretary to the MPC

- Deputy Director of Economic Research overseeing Money and Banking (Alternate Secretary, Head of Division, Money and Banking)

The primary function of the MPC is to evaluate emerging economic developments and macroeconomic projections and to make recommendations on appropriate future directions of monetary policy for consideration by the Monetary Policy Board with a view to achieving the primary objective of the Central Bank of ensuring domestic price stability.

The MPC meets at regular intervals, currently six times per year. At these meetings, members consider reports prepared by the Economic Research Department and other departments on monetary, foreign exchange market and price developments, together with developments in the fiscal, external and real sectors, which would serve as the bases for the deliberations of the MPC, in the formulation of recommendations to the Monetary Policy Board. At present, technical inputs provided by the Economic Research Department are based on comprehensive economic and monetary analyses including macroeconomic forecasts, particularly for inflation.

Stakeholder Engagement Committee (SEC)

The Stakeholder Engagement Committee (SEC) of the Central Bank of Sri Lanka (CBSL) was established in July 2022 by replacing the Monetary Policy Consultative Committee (MPCC) and the Financial System Stability Consultative Committee (FSSCC) of the CBSL which were in operation previously. The Committee consists of a cross-section of stakeholders including eminent professionals, academics, and private sector personnel so that the Central Bank benefits from their expertise and experience in its policy decision-making process.

Instruments/ Tools

OPR (Policy Rate)

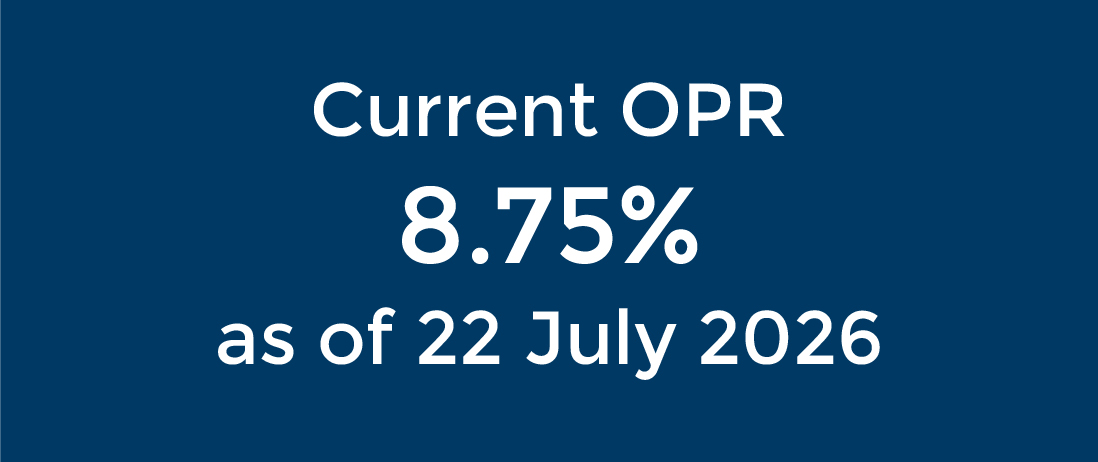

Overnight Policy Rate (OPR) is the policy interest rate of the Central Bank under the single policy interest rate mechanism (w.e.f. 27 November 2024). It is the primary monetary policy instrument that signals the Central Bank’s monetary policy stance. It serves as the benchmark interest rate for overnight transactions in the money market. OPR is periodically reviewed and adjusted appropriately, if necessary, by the Monetary Policy Board of the Central Bank, to guide the interest rate structure of the economy with a view to achieving the desired path of inflation.

Open Market Operations (OMOs)

The Central Bank conducts its monetary policy under a system of active OMOs within the Standing Rate Corridor (SRC) formed by the Standing Deposit Facility Rate (SDFR) and Standing Lending Facility Rate (SLFR), which are linked to OPR with a pre-determined margin set by the Monetary Policy Board, to manage liquidity conditions and maintain short-term interest rates at or around OPR.

OMOs are conducted either to absorb liquidity if there is excess liquidity, or to inject liquidity if there is a shortage of liquidity, thereby maintaining stability in short-term interest rates. OMOs are conducted through auctions to buy /sell government securities on a permanent or a temporary basis (Click here for a detailed description of the process of conducting OMO). The auction is on a multiple bid, multiple price system. Participants in the money market could make up to three bids at each short-term auction and up to six bids at each long-term auction and the successful bidders would receive their requests at the rates quoted in the relevant bid. The first step in the monetary policy implementation is liquidity forecasting. (Click here for the details)

The OMOs include a range of tools aimed at aligning market interest rates with the OPR. These tools include repurchase and reverse repurchase auctions, which involve liquidity injections and absorptions against collateral, and outright auctions, which involve the sale or purchase of government securities by the Central Bank from the secondary market. Each of these operations is strategically calibrated with OPR to ensure stability in market interest rates, thus reinforcing the monetary policy stance and monetary policy transmission. For overnight and short-term repo auctions, the Central Bank sets the OPR as the upper limit for bidding rates, while the SDFR serves as the lower bound. On the other hand, for reverse repo auctions, the range for bidding rates is established between the OPR and SLFR. The Central Bank allows the spread of bid rates for overnight and short-term auctions to fluctuate within this range, providing a controlled, yet flexible mechanism for liquidity adjustments.

Standing Facilities

Standing facilities are available for those participating financial institutions that were unable to obtain their liquidity requirements at the daily auctions. For example, if a participant has excess money even after an OMO auction, the participant could deposit such funds under the standing deposit facility at SDFR. Similarly, if a participant needs liquidity to cover a shortage, the participant could borrow funds on a reverse repurchase basis under the standing lending facility at SLFR. Accordingly, these facilities help contain wide fluctuations in overnight interest rates.

Statutory Reserve Requirement (SRR)

The Statutory Reserve Requirement (SRR) is the proportion of deposit liabilities that the Licensed Commercial Banks (LCBs) are required to keep as a cash deposit with the Central Bank. Under the CBA, LCBs are required to maintain reserves with the Central Bank at rates determined by the Bank. Demand, time and savings deposits of LCBs denominated in rupee terms are subject to SRR.

SRR has been widely used to influence the money supply in the past. However, the reliance on SRR as a regular monetary management measure has been gradually reduced with a view to enhancing the market orientation of monetary policy and also reducing the implicit cost of funds that the SRR would entail on LCBs. Therefore, at present, the Central Bank uses SRR to address persistent liquidity issues in the market (Click here for details on how SRR is computed).

Other Instruments

In addition, depending on the need and circumstances in the economy, the Central Bank can use quantitative restrictions on credit, ceilings on interest rates, moral suasion as well as communication and forward guidance for the purpose of monetary management.

Reports/ Publications

- Transparency

|

|

|

- Accountability

- Other

FAQ

What is Monetary Policy?

Monetary policy is the process by which the central bank influences the cost (i.e., interest rate) and availability of money (i.e., money supply/liquidity) with a view to attaining price stability.

Who is responsible for the conduct of monetary policy?

In Sri Lanka, the authority responsible for the formulation and implementation of monetary policy is the Central Bank of Sri Lanka (CBSL). With the enactment of the Central Bank of Sri Lanka Act (CBA) No. 16 of 2023, with effect from 15 September 2023, monetary policy decisions are taken by the Monetary Policy Board of the Central Bank.

The Monetary Policy Board is charged with the formulation of monetary policy of the Central Bank and implementation of a flexible exchange rate regime in line with the flexible inflation targeting framework in order to achieve its prime objective of maintaining domestic price stability.

The Monetary Policy Committee (MPC) of the CBSL, chaired by the Governor, is responsible for providing monetary policy recommendations to the Monetary Policy Board. The primary function of the MPC is to evaluate emerging economic developments and macroeconomic projections and to make recommendations on appropriate future directions of monetary policy for consideration by the Monetary Policy Board with a view to achieving the primary objective of the Central Bank of ensuring domestic price stability.

What is the current monetary policy framework of the CBSL?

At present, the Central Bank conducts monetary policy in line with a flexible inflation targeting (FIT) framework, aimed at maintaining inflation at the targeted levels as determined in the Monetary Policy Framework Agreement, while supporting economic growth to reach its potential.

The current Monetary Policy Framework Agreement between the Government and the Central Bank of Sri Lanka was published in the Government Gazette on 05 October 2023

What is flexible inflation targeting (FIT)?

Monetary policy conducted under a flexible inflation targeting (FIT) framework is aimed at stabilising inflation around the inflation target while minimising disturbance to the real economy. At present, the Central Bank conducts monetary policy in line with a flexible inflation targeting (FIT) framework, with the aim of maintaining inflation at 5 per cent as determined by the Monetary Policy Framework Agreement (MPFA) between the Minister of Finance and the Central Bank (Government Gazette).

What are the instruments used by the CBSL to conduct its monetary policy?

The Central Bank possesses a wide range of tools to be used as instruments of monetary policy. The main instruments are the Overnight Policy Rate (OPR), Open Market Operations (OMOs), Standing Facilities and the Statutory Reserve Requirement (SRR). In addition, quantitative restrictions on credit, ceilings on interest rates, moral suasion as well as communication and forward guidance can also be used. The Central Bank has the independence of choosing appropriate instruments to conduct monetary policy.

What is OPR?

Overnight Policy Rate (OPR) is the policy interest rate of the Central Bank under the single policy interest rate mechanism (w.e.f. 27 November 2024). It is the primary monetary policy instrument that signals the Central Bank’s monetary policy stance. OPR is periodically reviewed and adjusted appropriately, if necessary, by the Monetary Policy Board of the Central Bank, to guide the interest rate structure of the economy with a view to achieving the desired path of inflation.

Following the introduction of OPR, the use of the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) as policy interest rates were discontinued w.e.f. 27 November 2024. SDFR and SLFR, which are applicable for standing facilities of the Central Bank, are linked to OPR with a pre-determined margin set by the Monetary Policy Board. The SDFR and SLFR continue to provide the lower bound and upper bound, respectively, for interbank call money rates.

What is the Average Weighted Call Money Rate (AWCMR)?

AWCMR is a weighted average rate of interbank call money transactions, the overnight unsecured transactions among Licensed Commercial Banks (LCBs) and it serves as the operating target of the CBSL’s current flexible inflation targeting framework.

What are Open Market Operations?

Open Market Operations (OMOs) are the market based monetary policy operations conducted by the CBSL using acceptable securities to maintain market liquidity at appropriate levels in line with the monetary policy stance of the CBSL. The CBSL can use government securities and its own securities for this purpose.

What is the role of the Stakeholder Engagement Committee?

The Stakeholder Engagement Committee (SEC) consists of a cross section of stakeholders including eminent professionals, academics, and the private sector personnel. The primary role of this high-level consultative Committee is to represent the views and sentiments of the private sector and academia on economic conditions and the outlook, considering the overall economic development, particularly in the monetary and financial sectors of the economy. Further, SEC is expected to provide feedback from the viewpoint of the stakeholders of the economy on the policy measures adopted by the CBSL, thus enabling the CBSL to make informed policy decisions in a more consultative manner.

What are the key monetary aggregates in Sri Lanka?

The main definitions of monetary aggregates used in Sri Lanka are as follows;

- Reserve Money/Monetary Base/High Powered Money – Includes currency outstanding (currency held by the public and currency with LCBs), LCBs’ deposits with the CBSL and government agencies’ deposits with the CBSL.

- Narrow money (M1) - Includes currency held by the public and demand deposits held by the public with LCBs.

- Broad money (M2) – Includes narrow money supply and time and savings deposits held by the public with LCBs.

- Broad money (M2b) – Includes narrow money supply, time and savings deposits held by the public with LCBs and also includes a part of foreign currency deposits of LCBs.

- Broad Money (M4) - Includes broad money (M2b) supply and time and savings deposits held by the Licensed Specialised Banks (LSBs) and Licensed Finance Companies (LFCs).

What is the Average Weighted Lending Rate (AWLR)? / What is the Average Weighted Prime Lending Rate (AWPR)?

AWLR is calculated by CBSL, on a monthly basis, based on interest rates of all outstanding rupee loans and advances extended to the private sector by LCBs.

AWPR is calculated by CBSL, on a weekly basis, based on lending rates offered by LCBs to their prime customers during a particular week. A monthly average of weekly AWPR is also published.

What is the Average Weighted Deposit Rate (AWDR)? / What is the Average Weighted Fixed Deposit Rate (AWFDR)?

AWDR is calculated by CBSL, on a monthly basis, based on the weighted average rates of all outstanding interest bearing rupee deposits held with LCBs.

AWFDR is also calculated, on a monthly basis, by CBSL based on weighted average rates of all outstanding interest bearing rupee time deposits held with LCBs.

What is the Average Weighted New Deposit Rate (AWNDR)? / What is the Average Weighted New Lending Rate (AWNLR)?

AWNDR is calculated by CBSL, on a monthly basis, based on weighted average rates of all new interest bearing rupee deposits mobilised by LCBs during a particular month.

AWNLR is calculated by CBSL, on a monthly basis, based on interest rates of all new rupee loans and advances extended by LCBs to the private sector during a particular month.

What is the Legal/Market Rate of Interest?

The Legal Rate is defined under the Civil Procedure Code (Amendment) Act No. 6 of 1990 and is applicable to any action for the recovery of a sum of money. The Market rate is defined under the Debt Recovery (Special Provisions) Act No. 2 of 1990 and applies only in relation to actions instituted by lending institutions for the recovery of debt exceeding Rs. 150,000 arising out of commercial transactions, where there is no agreed rate of interest.

The Market Rate and the Legal Rate for a year are computed in December of the preceding year by the Central Bank and are announced through a Gazette notification.

What is the purpose of the monetary policy framework agreement between the Minister of Finance and the Central Bank of Sri Lanka?

A monetary policy framework agreement usually represents a formal agreement between the government, often led by the Ministry of Finance, and the country's central bank. Its primary objective is to create a structured framework for defining and adhering to a specific inflation target, which is a firm commitment shared by both the central bank and the government. This agreement plays a vital role in building trust and offering a well-defined path toward attaining macroeconomic stability.

The current Monetary Policy Framework Agreement between the Government and the Central Bank of Sri Lanka was published in the Government Gazette on 05 October 2023

What is the current inflation target, how to measure if the Central Bank has failed to achieve the inflation target, and what will happen if the Central Bank fails to meet the inflation target?

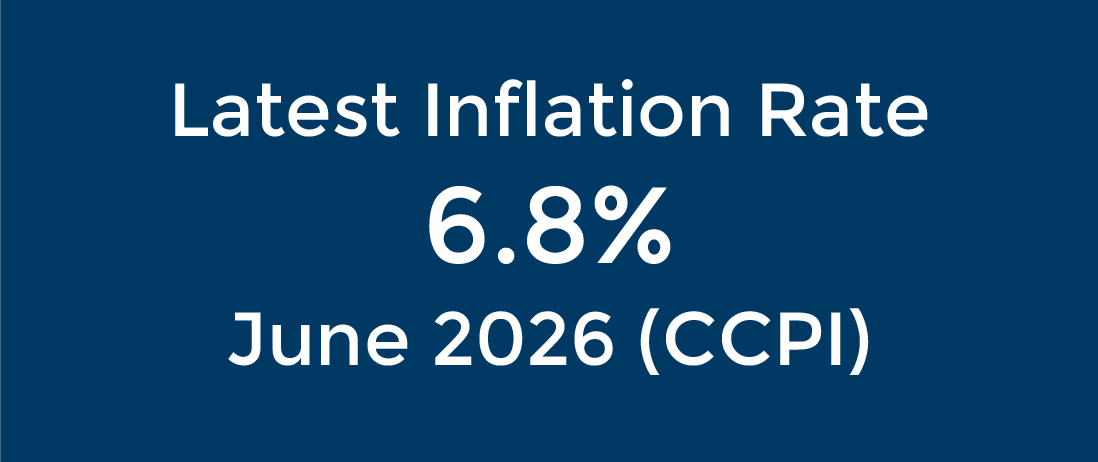

The current inflation target is to maintain the quarterly headline inflation rate at the target of 5 per cent. Here, the “Quarterly headline inflation rate” refers to the simple average of the year-on-year percentage changes in the monthly CCPI for the three months of the corresponding quarter, while “CCPI” means the Colombo Consumer Price Index published by the Department of Census and Statistics, Sri Lanka.

If the headline inflation rate deviates more than +/- 2 percentage points from the inflation target of 5 per cent for two consecutive quarters, the Central Bank is said to have failed to achieve the inflation target.

If the Central Bank has failed to achieve the inflation target, the Central Bank is obligated to submit a report to the Parliament through the Minister of Finance with the following information, which shall also be made available to the public.

(a) the reasons for the failure to achieve the inflation target;

(b) the remedial actions proposed to be taken by the Central Bank; and

(c) an estimate of the time-period within which the inflation target shall be achieved.